Because federal prohibition still throttles mainstream banking, U.S. dispensaries remain cash-heavy businesses. They safeguard revenue with a layered approach: smart safes and steel vaults on-site, armored-car pickups to cash vault facilities off-site, and niche cannabis-friendly banks or credit unions for final deposit. Here’s how the workflow really looks in 2025, what’s changing under the latest banking bills, and the security/compliance best practices every operator needs to know.

1. Why Dispensaries Handle So Much Cash

Even after the DEA’s proposed re-scheduling of cannabis to Schedule III, most national banks and the Visa/Mastercard networks still refuse plant-touching businesses. The bipartisan SAFE Banking Act has again passed the House but remains stalled in the Senate as of May 2025, leaving operators to rely on cash, closed-loop debit apps, or “cashless ATM” work-arounds. MarketWatch GreenGrowth CPAs

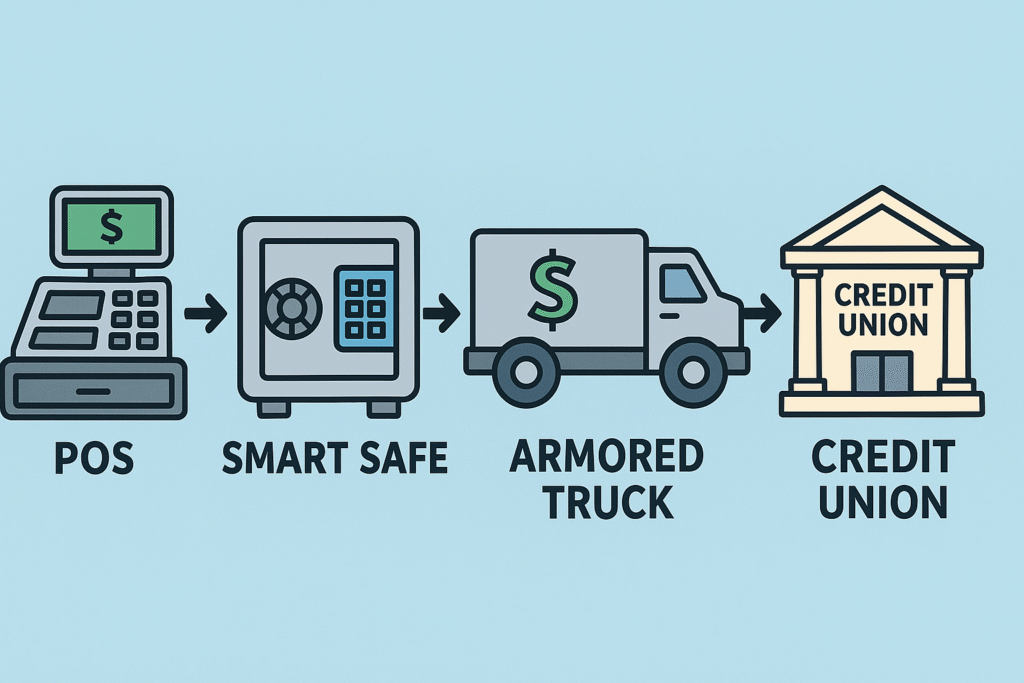

2. The Typical Cash Journey — Step by Step

| Step | Where the Cash Sits | Key Gear / Partners | Risk It Solves |

|---|---|---|---|

| Point-of-Sale | Under-counter drop boxes or cash tills | Reinforced POS drawers that slot into a safe below the counter | Snatch-and-grab theft |

| End-of-Shift | Smart safe in the back room | Validates bills, auto-counts, logs deposits, and lets managers create provisional bank credits | Internal shrinkage, counting errors (Sapphire Risk Advisors, cannabistech.com) |

| Daily/Weekly | UL-rated steel vault or modular vault room | Heavy-gauge steel, dual-control locks, 24/7 CCTV | Armed robbery, overnight break-ins |

| Transport | Armored-car pickup | Cannabis-specialized carriers (e.g., Empyreal, RapidArmored) | Transit robbery, federal civil-asset-forfeiture risk |

| Final Deposit | State-chartered bank / CU or cash-vault service | Institutions compliant with FinCEN cannabis SAR rules; vault services operated by payment processors | Permanent off-site security, audit trail (Goodwin Law, Flowhub) |

3. Deep Dive: On-Site Storage Options

Traditional Drop Safes

Cost-effective, quick install.

No bill validation—relies on manual counts.

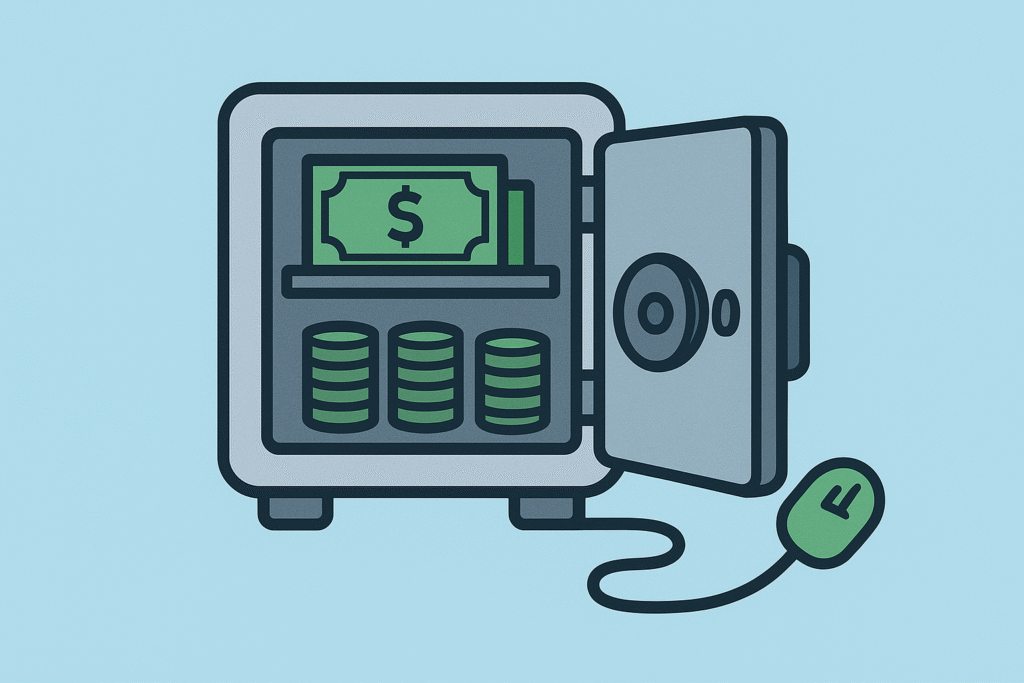

Smart Safes (2025’s Go-To)

Equipped with billvalidators, connected software, and audit logs.

Can extend provisional credit with select banks before physical pickup, improving cash flow.

Saves ~200 labor-minutes per register each week but comes with subscription/data fees. Convenience

Modular Vault Rooms

Scalable steel panels; can meet UL-291 or GSA specs.

Recommended once daily cash volume regularly tops $150K.

Greenboost Tip: Smart safes pay for themselves fastest when you pair them with an armored-car service that scans the safe’s audit data remotely. Negotiate for lower pickup frequency once bill validation is digital.

4. Off-Site “Cash Vault” Services

Payment processors and ATM providers sometimes run their own cash-vault facilities. Funds arrive via armored-car, get counted under dual control, and post to your merchant account within 24 hours. Some dispensaries opt for this when local credit-union branch access is limited—or when they’re using cashless ATM setups that require vault reconciliation. Goodwin Law

5. Banking Work-Arounds That Aren’t a Safe

| Work-Around | How It Works | 2025 Reality Check |

|---|---|---|

| Cashless ATMs | POS mis-codes a sale as a cash withdrawal | Networks are cracking down; expect widespread shutdowns this year. (Talking Joints Memo) |

| Closed-Loop Debit (e.g., CanPay) | Customer links checking account; transaction runs on private rails | Growing, but fees still higher than mainstream debit. |

| Fintech “Sweep” Accounts | Processor sweeps cash into FDIC-insured partner banks nightly | Compliance scrutiny rising; read the fine print. |

6. Compliance & Security Best Practices

Follow FinCEN Guidance to the Letter

Maintain KYC on every owner/investor.

Provide seed-to-sale and cash-handling records to your bank quarterly.

Dual Control + Time-Delay Locks on every safe.

Daily Reconciliation With POS to catch skims early.

Insure Your Cash in Transit — many general liability policies exclude cannabis.

Arm Your Data Too: Smart-safe logs, CCTV footage, and armored-car manifests should all flow into a secure, cloud-based drive with 256-bit encryption.

7. What Could Change Soon?

SAFER Banking 2.0 (new Senate draft) aims to give FDIC-insured banks explicit safe harbor; hearings are expected again this summer. Marijuana Moment

Rescheduling to Schedule III may ease IRS burdens (280E relief) but won’t alone bring Visa/Mastercard online.

Several states—Colorado, New York, Illinois—are piloting public-banking models dedicated to cannabis. Watch for lower fees but stricter audits.

Final Takeaways for Operators & Investors

Dispensaries keep their cash wherever layered security, bank compliance, and cash-flow timing intersect. In 2025 that usually means:

Smart safe + nightly vault in-store

Armored-car pickup 1–3× per week

Deposit with a cannabis-friendly credit union or cash-vault partner

Stay agile: monitor federal legislation, renegotiate armored-car contracts annually, and audit your smart-safe data weekly. Master those three levers and you’ll lower theft risk, improve liquidity, and impress the compliance auditors — all while freeing up capital to reinvest in growth.

Need a deeper audit of your dispensary’s cash-flow and compliance stack? Greenboost’s cannabis-centric finance and POS experts are one call away. Let’s turn a cash challenge into your next competitive edge.